A New Frontier in P2P Borrowing: Fixed or Variable?

In the ever-evolving landscape of peer-to-peer (P2P) lending, borrowers and investors face an important crossroads: choosing between fixed and variable interest rates. Each option carries distinct advantages and risks, and the decision can have profound implications for your financial outcomes. Whether you’re a first-time borrower exploring personal financing or an investor eager to maximize returns, understanding how fixed and variable rates operate in P2P ecosystems is crucial. In this comprehensive guide, we’ll unravel the mechanics behind each structure, spotlight real-world considerations, and empower you to make informed decisions that align with your goals.

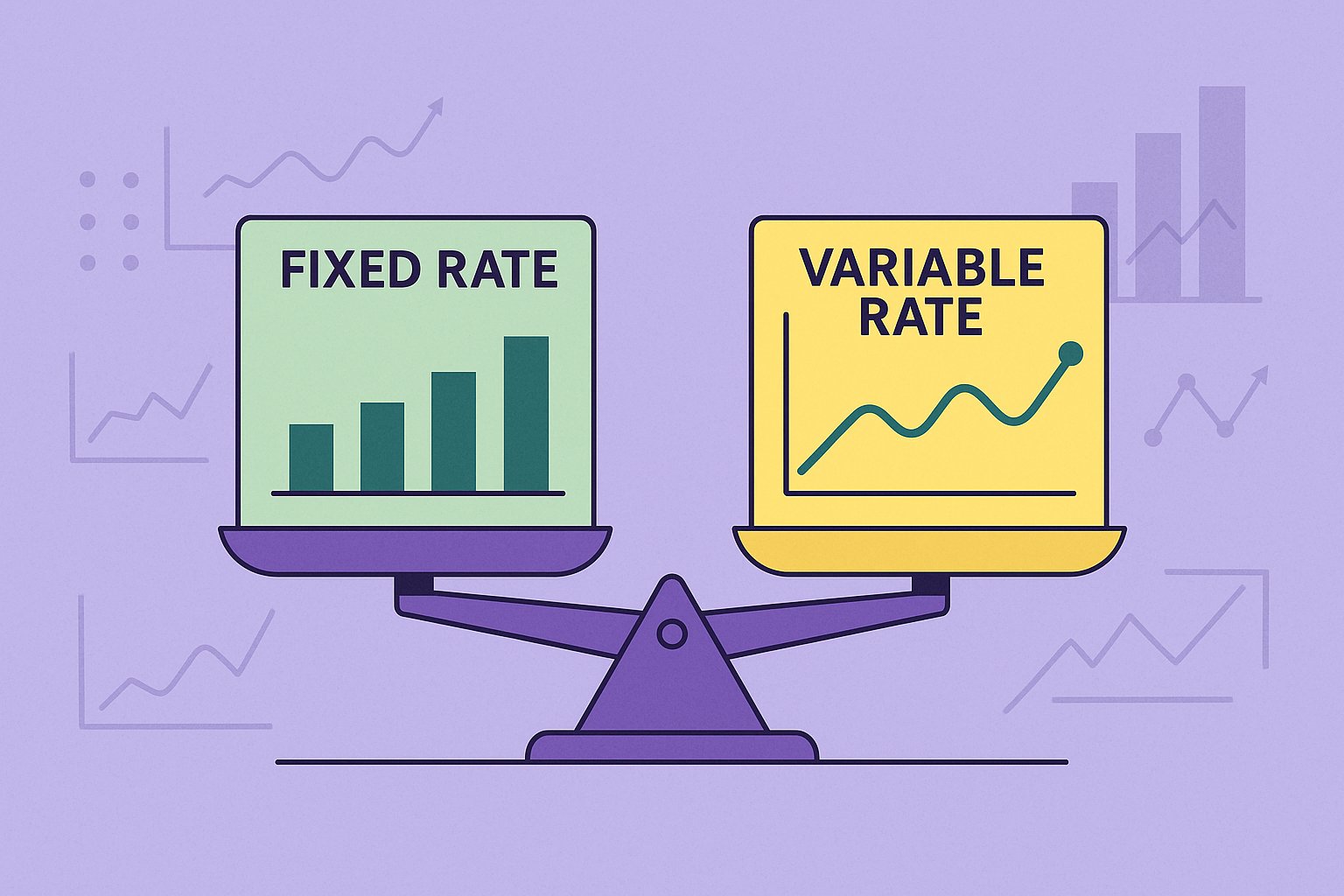

The Essence of Fixed-Rate Lending

Fixed-rate loans in P2P platforms offer one of the most appealing features: predictability. Once your loan is funded, the annual percentage rate (APR) remains unchanged for the entire term. This means borrowers can budget confidently, knowing exactly what their monthly payments will be. From six-month personal loans to five-year small business notes, a fixed rate translates into unwavering stability. Investors, too, benefit from forecasting returns with precision. When you fund a fixed-rate note, you receive a consistent yield, regardless of market fluctuations. For many participants, especially those risk-averse or operating within tight monthly cash-flow constraints, the certainty of a fixed rate brings peace of mind. No unexpected spikes in interest can derail a borrower’s repayment plan, and investors won’t be blindsided by sudden contractions in yield.

Unpacking the Variable-Rate Equation

In contrast to the unchanging nature of fixed APRs, variable-rate P2P loans pivot according to predetermined benchmarks—often tied to the prime rate or a platform-specific index. When market conditions shift, the interest charged to borrowers may go up or down periodically. For example, a loan might start at 7.5% APR for the first year, then adjust annually based on the underlying reference rate plus a margin. Borrowers who choose variable rates essentially place a bet on future market behavior; if benchmark rates drop, their interest cost could decrease accordingly. Conversely, rising rates could translate into steeper monthly payments. From the investor’s perspective, variable-rate notes can be tantalizing during periods of rising interest rates, since their yields adjust upward in line with broader market movements. Yet this upside potential comes with volatility: investors must be prepared to see returns recede when rates tumble.

Real-World Implications for Borrowers

For many P2P borrowers—especially those new to digital lending platforms—the simplicity of a fixed-rate loan offers a compelling entry point. Picture a recent graduate seeking $15,000 to consolidate credit card debt: the fixed-rate model ensures that whether inflation picks up or the economy softens, monthly obligations remain unaltered. Budgeting becomes straightforward, and there are no surprises on payment day. On the other hand, a borrower who anticipates falling interest rates—perhaps due to central bank signals or economic downturns—might lean into a variable-rate option to capitalize on lower borrowing costs over time. Startups and small businesses with flexible cash flow can also embrace variable rates, viewing them as a strategic hedge. If revenues rise faster than interest adjustments, the net effect can be beneficial. However, borrowers must vigilantly monitor macroeconomic shifts; during a sudden interest rate upswing, their monthly payments could climb sharply, straining budgets and jeopardizing debt repayments.

Investor Perspectives: Balancing Yield and Volatility

Investors in P2P platforms often weigh the trade-off between the steady appeal of fixed-rate notes and the promise of enhanced returns that variable-rate loans can deliver when rates accelerate. Consider an investor who allocates $10,000 to fixed-rate loans at an average yield of 7%. They can project exactly $700 in annual interest, minus any defaults. Conversely, if that same $10,000 is split across variable-rate notes starting at 6%, the investor stands to benefit if benchmark rates rise to push the yield to 8% or 9%. This dynamic positions variable-rate notes as a potentially lucrative play during periods of rate normalization. Yet, with downside risk baked in—if rates fall to 4%, variable notes suffer—the investor must accept a degree of uncertainty. To manage this, many seasoned P2P lenders diversify across both fixed and variable instruments, creating a blended portfolio that offers cushion against rate gyrations while still capturing some upside when markets tilt upward.

How Economic Backdrops Shape Rate Decisions

No loan exists in a vacuum, and the broader economic environment plays a pivotal role in determining which rate structure thrives. During low-rate environments—characterized by aggressive central bank interventions or recessionary headwinds—fixed-rate loans often become incredibly attractive. Investors scour platforms for any opportunity to lock in yields above zero, and borrowers rejoice at the prospect of securing long-term financing at historically low APRs. Conversely, when economies heat up and policy makers pivot to tame inflation, interest rates can climb swiftly, making variable-rate notes a more enticing bet for those who believe rates will continue rising. Timing is everything: borrowers who locked in fixed rates at the onset of a tightening cycle may inadvertently secure financing at a rate well below the new market norm. Variable-rate holders, however, might see their loan costs escalate, prompting borrowers to refinance into fixed-rate tranches if possible. Understanding economic signals—such as inflation reports, employment data, and central bank guidance—helps both borrowers and investors anticipate rate trends and calibrate their P2P strategies accordingly.

Weighing Early Repayment and Prepayment Risks

Another nuance that often separates fixed and variable-rate loans is the handling of prepayments. Many fixed-rate loans in the P2P space come with prepayment penalties to safeguard investors: if a borrower repays their loan early, they might owe a small percentage of the remaining interest as a liquidated damages fee. This structure helps investors recoup lost interest that would have been paid over time. By contrast, variable-rate loans frequently waive prepayment penalties, encouraging borrowers to pay down principal when they can. For borrowers, this feature can be empowering: an unexpected windfall—such as a bonus or inheritance—can accelerate debt payoff without incurring additional fees. However, from an investor lens, penalty-free prepayments introduce uncertainty in projected cash flows. When borrowers pay off early, funds return to the marketplace, and investors must find replacement notes—sometimes at lower yields. Savvy P2P lenders, therefore, analyze historical prepayment rates for each loan type, factoring these behaviors into expected return models.

Credit Grade Interactions: Fixed vs Variable

P2P platforms typically assign borrowers a credit grade—ranging from A to G—based on credit scores, income, and other risk metrics. Fixed-rate loans generally democratize credit grades into predetermined APR buckets: an A-grade note might carry 6% APR, while a D-grade frets 12%. Variable-rate loans, however, layer dynamic pricing atop credit grades. For instance, a B-grade borrower could start with a 7% variable rate pegged to the prime rate plus a margin. If the prime rate climbs by 1%, the APR jumps to 8%. As a result, variable-rate borrowers with lower credit grades face compounding risk: not only do they occupy a higher starting rate, but any macroeconomic shifts amplify their cost of borrowing. Alternatively, investors eyeing high-grade variable notes can anticipate modest rate bumps that still keep default risks low. Ultimately, credit grade amplifies or dampens the core tensions inherent in fixed versus variable structures, making it essential for platform participants to scrutinize how each loan’s grade influences interest behavior over time.

Strategic Considerations for Portfolio Diversification

Given the inherent trade-offs between fixed and variable rates, many P2P investors adopt a balanced approach. Allocating a portion of capital to fixed-rate notes delivers stable, predictable returns—safeguarding against sudden economic downturns. The remaining slice of the portfolio can target variable-rate loans, poised to capture incremental yield if market rates tick upward. By blending these instruments, investors effectively create a built-in hedge: when fixed-rate notes underperform in rising rate environments, their variable counterparts may rally, mitigating overall portfolio volatility. Borrowers, too, can use diversification strategies at the individual level. For example, a small business owner might split their funding need between a five-year fixed-rate P2P loan to cover facility renovations and a variable-rate loan for short-term inventory financing. This structure allows the business to lock in stable costs on long-term assets while retaining flexibility to repay or refinance shorter-term obligations as market conditions evolve.

Tips for Borrowers: Making the Right Rate Choice

Choosing between fixed and variable APRs hinges on personal or business circumstances. If your revenue streams are steady and predictable—such as a salaried income or a subscription-based business model—locking in a fixed rate secures consistent monthly obligations and eliminates worries about future payment spikes. Conversely, if you anticipate substantial revenue growth, intermittent cash surges, or exposure to inflation-adjusted pricing, a variable rate may unlock savings if central bank policy eventually slides rates downward. Borrowers should also pay close attention to the loan’s adjustment schedule: how frequently does the rate reset? Is there a rate cap that prevents dramatic APR escalations? Understanding these guardrails helps avoid sticker shock. Finally, always compare the APR “floor” (the lowest possible rate) and the “ceiling” (maximum allowable rate) for variable loans. Together with a clear-eyed view of your cash flow projections, these details empower borrowers to choose the rate structure that maps onto their risk tolerance and growth expectations.

For Investors: Seamlessly Integrating Fixed and Variable Notes

If you’re an investor immersing yourself in the P2P realm, start by delineating your core objectives: are you chasing absolute yield, or is capital preservation paramount? For conservative strategies, a heavier allocation to fixed-rate loans cements stable returns, while a smaller variable allocation offers a tactical way to capitalize on rising rates. Yet if your risk appetite is higher—perhaps you’re comfortable weathering periods of market volatility—you might tilt the scales slightly toward variable notes, especially if forward-looking indicators suggest tightening monetary policy. Whichever route you choose, monitor economic headlines closely: announcements from the Federal Reserve or similar central banks often foreshadow shorter-term rate movements that can influence your returns. Additionally, review the platform’s historical performance metrics: what percentages of variable-rate loans have experienced year-over-year interest adjustments, and how have borrower default rates evolved as rates changed? This data-driven approach ensures that your investment mix not only reflects your macroeconomic view but also responds to real-world borrower behaviors and platform dynamics.

Charting Your Path: Conclusion and Next Steps

As peer-to-peer lending continues to disrupt traditional financial paradigms, the clash between fixed and variable interest rates remains at the heart of borrower and investor decision-making. Fixed-rate P2P loans deliver unwavering stability, shielding participants from market volatility and simplifying budgeting processes. Variable-rate loans, on the other hand, offer the tantalizing prospect of capturing rising yields—offset by the inherent unpredictability of economic cycles. Neither model reigns supreme; rather, each serves distinct financial objectives. By dissecting credit grades, prepayment behaviors, and broader economic trends, you can craft a tailored strategy that harmonizes with your unique goals. Whether you’re seeking to consolidate debt, finance a startup, or build a diversified P2P investing portfolio, mastering the nuances of fixed versus variable rates is your gateway to sustained success. The future of peer-to-peer lending belongs to those who understand how interest terms shape risk and reward—so embrace the lessons, analyze the data, and make your next move with confidence.